Truckers slammed the brakes on their budgets this week. Diesel prices rocketed 96 cents a gallon—the biggest weekly leap since records began in 1994. And guess who’s footing the bill? You, the shipper, through fuel surcharges that carriers love to game.

Zoom out: this isn’t some blip. The U.S. Energy Information Administration pegged the average on-highway diesel at $4.859 for the week ended March 9—a 25% surge. Paul Berger nailed it in the Wall Street Journal:

“Diesel prices for U.S. truckers rose a record 96 cents a gallon this past week, an ominous sign for retailers and manufacturers juggling tariffs and bracing for higher shipping costs following the U.S.-Israeli attacks on Iran.”

Ominous? Understatement. We’re staring down volatility fueled by Middle East flare-ups, and shippers are caught flat-footed.

Carriers’ Favorite Cash Grab

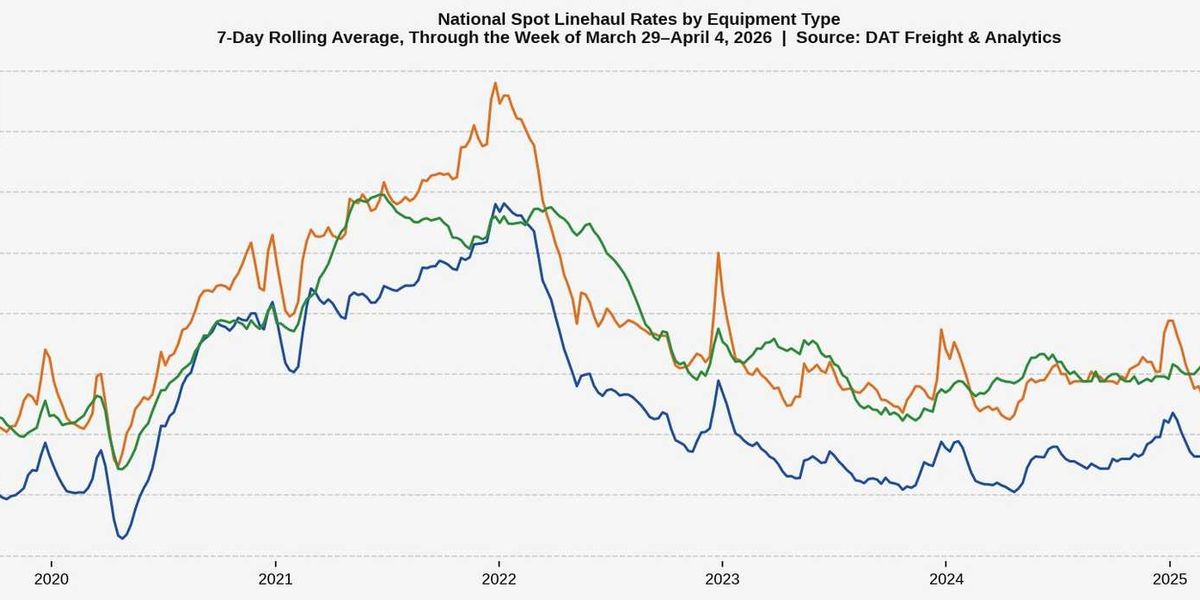

Flashback to 2022. Diesel hit $5.134 a gallon. Sound familiar? I covered the last oil shock waves—remember the ’70s embargo? Same playbook: geopolitics jacks prices, everyone panics, carriers cash in. Back then, we polled supply chain execs in our Indago community. Half had standardized fuel surcharge programs—using a common index, base rate, escalator. Sound good? Not really. Fifteen percent admitted wild variations by carrier; twenty percent? Clueless or ‘other.’

One exec spilled the beans:

“Fuel surcharges [FSC] are 100% profit makers for carriers. For truckload carriers, despite the matrix I ask them to use, it’s a bottom-line price they look for and if we don’t ‘give in’ we don’t get equipment… FSC were meant to compensate carriers for their added costs of fuel. Years ago, and well into today, it’s a profit center for them.”

Bingo. That’s my unique take here—no one’s saying it loud enough: fuel surcharges started as fair play, but they’ve morphed into carrier slush funds. Shippers ‘set it and forget it,’ while truckers tack on extras that don’t match real costs. Who audits the escalators? Crickets.

Others griped about manual tools that lag, 3PLs hiding the ball, or pushing alt-fuels for green cred. Noble, but diesel’s king for now—trucks guzzle 90% of U.S. fuel.

Short para. Cynical truth: carriers win.

Are Your Fuel Surcharges Ready for $5 Diesel?

Four years ago, 45% planned no changes. Twenty percent eyed bigger escalators—dumb move, hands profit to carriers. Others wanted market-based indexes or more standardization. Smart? Ish. But volatility’s back, baby. Tariffs loom, Iran’s rattling sabers—prices could kiss $5 again by summer.

Here’s the thing—and this is my bold prediction, unseen in the original WSJ piece: this spike forces a modal shift. Rail’s capacity-starved, but intermodal could steal 10-15% of truck volume if diesel holds over $4.50. Carriers know it; that’s why they’re squeezing FSCs now. Shippers asleep? Expect margin Armageddon.

Look, I’ve watched Silicon Valley hype autonomous trucks as saviors since 2010. (Waymo’s still puttering.) Same with electrification—Tesla Semi’s a tease. Real fix? Dynamic surcharges tied to real-time indices, AI-monitored for gouging. But most orgs? They’ll whine, pay up, repeat.

One respondent nailed the inertia:

“We ‘set it and forget it’ — we should see what others are doing.”

Yeah, do that. Before it’s too late.

Why Carriers Laugh Last

Break it down. Fuel’s 30-40% of truck costs at these levels. Surcharges should cover it—transparently. Instead? Carriers blend base rates low, FSCs high. Shippers see total linehaul balloon without questioning. Our 2022 poll showed 3PLs botching visibility. Still true? Bet on it.

Geopolitics amps this. U.S.-Israel-Iran mess? Oil futures twitched 5%. Add Red Sea disruptions—shipping reroutes balloon truck demand. Result: spot rates spike, FSCs follow. Retailers, manufacturers: your Q2 forecasts? Trash ‘em.

But. Alternatives bubble up. High prices spur LNG trucks, battery swaps. Sustainability? Sure, but capex kills it short-term. Carriers push back—why switch when diesel desperation pays their bills?

Wander a sec: I once grilled a carrier CEO post-2022 peak. ‘FSCs are negotiated,’ he smirked. Negotiated—with capacity tight, shippers fold. Classic.

Ditch the Dinosaur Programs

Revamp now. Standardize indexes (use EIA weekly). Cap escalators at actual cost-plus. Audit quarterly—tech like FourKites or project44 flags anomalies. No more ‘set and forget.’

Prediction holds: if prices stick, 20% of shippers shift modes by year-end. Rest? Bleed cash. Who makes money? Carriers, brokers, index providers. Shippers? Suckers—unless you wise up.

Long para done. Action item. Review today.

🧬 Related Insights

- Read more: Shipments Snagged at the Dock: U.S. Tariff Enforcement Hits Overdrive

- Read more: CBP Tariff Refunds Now Dragged to 60-90 Days: The Supply Chain Squeeze Tightens

Frequently Asked Questions

What causes sudden diesel price spikes?

Geopolitical shocks—like U.S.-Israel strikes on Iran—plus supply crunches and demand surges from trucking. EIA tracks it weekly.

How do fuel surcharges work in trucking?

They’re add-ons based on diesel indexes (e.g., EIA), with base rates and escalators. Meant to pass real fuel costs—but often padded by carriers.

Should I update my fuel surcharge program now?

Yes, if it’s static or carrier-varying. Go dynamic, standardized, audited—or watch margins evaporate as diesel climbs.