Air freight? Miles from normal.

That’s the stark verdict from analysts as the US-Iran ceasefire fails to dent a market gripped by fuel spikes and network chaos. Forget quick rebounds—Maarten Wormer, head of consulting at Aevean, just laid it out plain on The Loadstar podcast: we’ve shaved six percentage points off expected global growth. Start of the year? 5-6% bump. Now? One point already gone, and that’s before counting the real pain ahead.

Why Fuel Costs Are Crushing Everyone

Jet fuel in Asia? 160% pricier than last year. Tankers to Europe? Forty days minimum. Wormer nails it:

“Normalisation is still very, very far away… fuel is one of the big drivers,” he said, noting tanker shipments to Europe could take up to 40 days. “In Asia, jet fuel prices are around 160% higher than last year… that will take way more than the two-week ceasefire to normalise.”

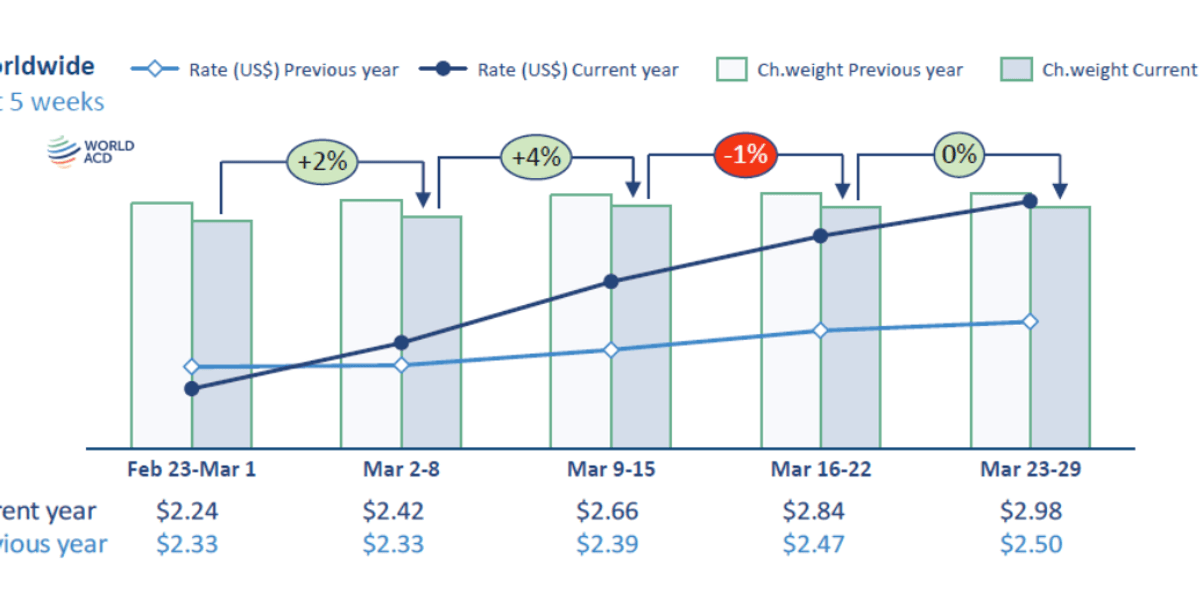

Spot rates from Hong Kong to Europe? Shooting up through March. India-Europe? Doubled outright. Not demand—supply squeeze. Baltic Air Freight Index jumped 25% in four weeks to early April. Peak season vibes, minus the seasonal cheer.

Here’s the data twist nobody’s hyping: March flipped the script. Cargo Facts calls it an inflection point—geopolitics, fuel, constraints now rule over old seasonality. Rotate’s capacity charts? Year-on-year growth nosedived negative. Middle East routes tanked double-digits; Asia-Europe and transpacific clawed back gains.

A single brutal fact.

Global freighter capacity rose 9% month-on-month in March—but effective supply? Way tighter. Airlines reroute, add 15-20% detours at peak disruption. Even with some capacity trickling back, longer hauls mean less bang for the buck.

Is Rerouting a Real Fix or Just a Band-Aid?

Traders aren’t mincing words. “Normally we would route everything via the Middle East,” one told TAC Index. “Now there is less flexibility, transit is longer and costs are much higher.”

Asia-Europe wins big—direct flights, secondary hubs like Anchorage, even Central Asia popping. Airlines pivot to pricing power zones. Freighters from Atlas Air, FedEx, Cargolux plug bellyhold gaps from passenger cuts.

But Asia-North America? Soft demand plus policy fog. Perishables hurt worst—low value density can’t take fuel hikes. E-commerce squeezes next. High-end stuff like data center gear? They’ll shrug it off.

My take—and here’s the angle the headlines miss—this echoes the 1973 oil embargo, but airborne. Back then, crude quadrupled; airlines slashed flights, rates exploded. Today? Jet fuel doubles amid refining squeezes, but we’ve got e-commerce ballast. Prediction: by Q3, if Iran tensions simmer, we’ll see trucking landbridges bloom across Central Asia, turning freight into a hybrid beast. Not hype—pure market math.

Rates scream supply pain.

Will This Crush Low-Margin Shippers?

Volatility’s the new boss. Capacity fragmentation everywhere—by region, hub, commodity. DHL leads the race; DSV treads water; FedEx pushes marketing amid labor pacts.

Corporate spin calls it adaptation. Bull. It’s survival mode. XOM updates war impacts; Maersk tweaks estimates fairly. But CHRW? Just a bad week. WTC on a roller coaster.

Look, networks reconfigure fast—that’s air freight’s edge over ocean. But rebuilding trust? Months. Fuel normalization? Quarters, if crude chills. And that Strait of Hormuz bypass chatter—trucking landbridges sound clever, until you price the CO2 and delays.

Shippers, hedge now. High-value cargo holds; everything else braces.

One overlooked parallel.

1973’s embargo killed airline expansion for years. We’re not there—freighters grew—but don’t bet on smooth skies. Ceasefire’s a pause, not a fix. Expect rates 20-30% above norm through summer, barring miracles.

🧬 Related Insights

- Read more: El Niño’s Shadow Falls on Panama Canal — Low Water Looms Again

- Read more: Iran’s Strait Deadline Lights Fuse Under Oil Routes and Stock Markets

Frequently Asked Questions

When will air freight normalize after ceasefire?

Not soon—fuel prices need months to settle, networks quarters to stabilize.

How is Middle East conflict hitting air freight rates?

Reroutes and fuel spikes doubled some lanes; capacity down 15-20% effectively.

Are air freight capacity gains real or illusion?

Nominal up 9%, but longer routes make it feel tighter—volatility reigns.