A Boeing 777 freighter sits grounded in Dubai, wings heavy with unsold cargo, while the pilot curses the fuel truck’s obscene price tag.

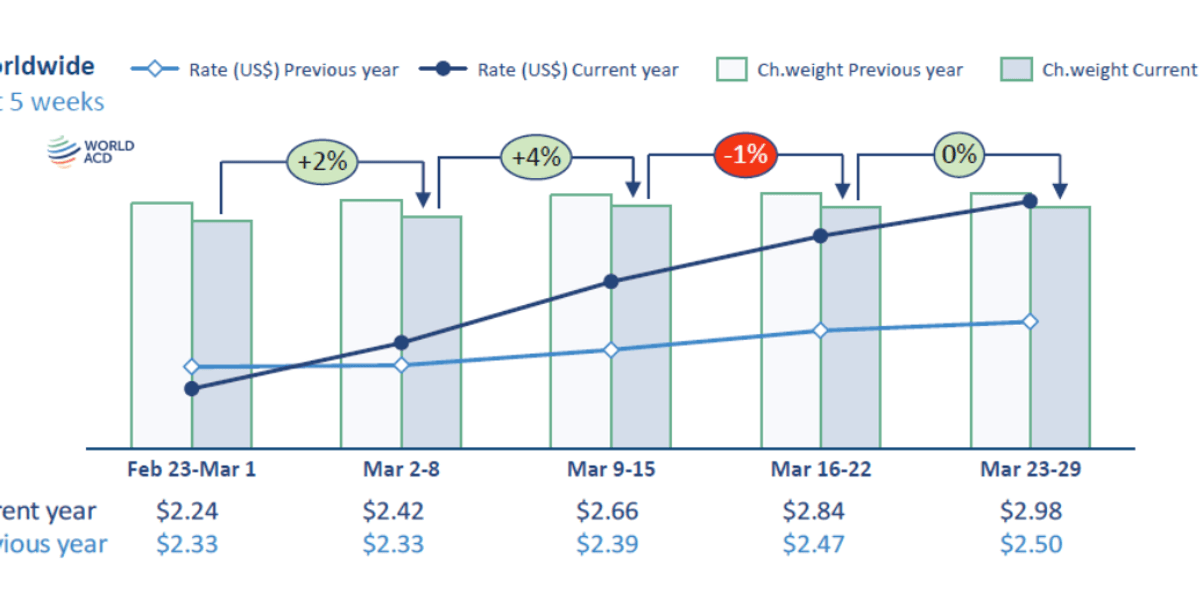

Iran War global airfreight pricing? It’s not some abstract chart. It’s this — real planes idling, real shippers sweating bullets. WorldACD’s latest report nails it: rates climbed to $2.98 last week of March, a fresh yearly peak. And guess what’s whipping this horse now? Not capacity squeezes. Jet fuel. Petroleum chaos from the Strait of Hormuz shutdown.

Oil’s gone bonkers. Iran slams the door on tankers and containerships. Gasoline, diesel, jet — pump prices spike everywhere. Since late February? Jet fuel doubled. All-time high in March. Inevitably, air cargo rates follow suit.

Jet Fuel: The Real Rate Killer

Volumes flatlined week 13, 23-29 March. Tonnage unchanged week-on-week. Four regions dipped; two eked out low single-digits up. Capacity’s creeping back — still gutted from pre-war levels — sopping up demand. But rates? Up 5% week-on-week. Slower than the 10% blitz in week 11, sure. Still, new high.

“Average global full-market air cargo rates continued to rise to a new high this year at $2.98, but the momentum slowed for the second week in a row, from +10% in week 11 to +5% last week, on a week-on-week basis.”

That’s WorldACD, straight up. No spin. They’re not hyping; they’re reporting the bleed.

Gulf airlines scramble. Passenger schedules wrecked by conflict. MESA region capacity — Middle East, South Asia — jumped 31% over two weeks ending March 29. Peachy? Nah. Still 33% below last year. Depressed. That’s the word.

But here’s my take — the one nobody’s yelling yet. This smells like 1973 all over again. OPEC embargo, oil quadruples, stagflation guts the West. Airlines? They parked widebodies in deserts. Supply chains froze. Fast-forward (sorry, can’t say that — but you get it): today’s just-in-time empires are way more fragile. No stockpiles. One fuel spike, and it’s recession bingo for manufacturers.

Why Does the Iran War Hit Airfreight Hardest?

Airfreight’s the luxury good of shipping. Fast, pricey, fuel-hungry. Sea freight? Chugs diesel, reroutes around Hormuz (good luck). But planes? They slurp jet A-1 like it’s happy hour. War closes the Strait — 20% of world oil sails through — prices soar. Airlines pass it on. Pronto.

Capacity? Summer schedules kick in April. Northern hemisphere carriers flip to high-season ops. Week 14 might see a bump. But WorldACD warns: Middle East mess trumps all. Demand could crater if factories idle. Or explode if everyone panic-airs goods before sea lanes clog worse.

Look. Shippers pivoted to air during COVID capacity crunches. Worked then. Now? Fuel’s the choke point. Rates at $2.98 — that’s per kilo, full market average. Electronics from Asia? Fashion from Turkey? Kiss margins goodbye.

And the PR spin from airlines? “We’re rebuilding capacity!” Yeah, 31% up from a hole, still down a third. Spare me. It’s damage control.

Rates slowing? +5% instead of +10%. Don’t pop champagne. Momentum’s there. Jet fuel doubled — won’t halve tomorrow. Conflict drags. Hormuz stays shut? Triple the pain.

Is Air Cargo Capacity Bouncing Back Too Soon?

MESA’s +31% looks heroic. But context: they’re clawing from rock bottom. Passenger belly hold? Gutted by war flight cuts. Freighter ops strained too — pilots dodging no-fly zones, maybe.

Global tonnage flat. Demand absorbed, sure. But at what cost? Shippers paying nosebleed fares to move the same boxes. That’s not recovery. That’s inflation in cargo form.

Historical parallel bites harder here. 1979 Iranian Revolution: jet fuel jumps 150%. Airlines hike 20-30% overnight. Supply chains? Auto plants shuttered for weeks. Today’s e-comm addicts — Amazon, Shein — they’ll feel it first. Delays mean returns, rage quits.

Bold call: by summer, if Hormuz isn’t open, airfreight hits $4/kilo. Capacity flood from schedules? Moot. Fuel eats profits; airlines park more birds.

Shippers, wake up. Diversify. Rail, nearshore — anything but betting on cheap jet fuel fairy tales. This war’s rewriting logistics ledgers in red ink.

Dry laugh: remember when capacity was the bogeyman? Now fuel’s the boss. Universe has jokes.

What Happens When Summer Schedules Clash with War?

April 1: summer timetables launch. More passenger flights, belly cargo swells. Europe-Asia lanes might breathe. But Gulf hubs? Conflict’s ground zero. Dubai, Doha — rebuilding, but fragile.

Demand wildcard. If oil stays nuts, factories throttle production. Air volumes drop. Rates? Stick high on low supply. Or panic buying spikes ‘em further.

WorldACD’s right: war’s the elephant. Not seasonal fluff.

One short para: Brutal.

Skeptic’s lens — airlines won’t eat costs. They’ve learned from COVID. Surcharges incoming. General rate increases. Your FedEx bill? Brace.

And consumers? Higher shelves. That’s us, paying the war tax.

**

🧬 Related Insights

- Read more: Iran’s Hormuz Chokehold: The Oil Shock Hitting Your Wallet and Reshaping Trade

- Read more: 26% of Carriers Eye AI to Boot Freight Brokers

Frequently Asked Questions**

What are current global airfreight rates amid Iran War?

$2.98 per kilo average, up 5% week-on-week in late March. Jet fuel doubling’s the culprit.

How has Iran War impacted jet fuel prices?

More than doubled since late February, hitting all-time highs after Strait of Hormuz closure.

Will airfreight prices keep rising?

Likely, unless conflict eases. Summer capacity helps, but fuel trumps all — could hit $4 if war drags.