Shipper in Shenzhen, phone buzzing. Rates from China to L.A.? Up 50% overnight. Jet fuel’s doubled since February. And that’s before the Strait of Hormuz whispers turn to shouts.

Global freight markets rocked by Iran War effects—Dimerco Express Group’s April 2026 Asia-Pacific Freight Report nails it. Fuel shock. Tighter air capacity. Hormuz disruptions. Not some vague demand wave, but hard, reroute-forcing pain.

Zoom out. Manufacturing’s still growing worldwide—China’s factories hum, Taiwan pumps out chips—but softer now, squeezed by costs that bite deeper than any post-pandemic surge.

How Did Jet Fuel Jump from $95 to $197 in Weeks?

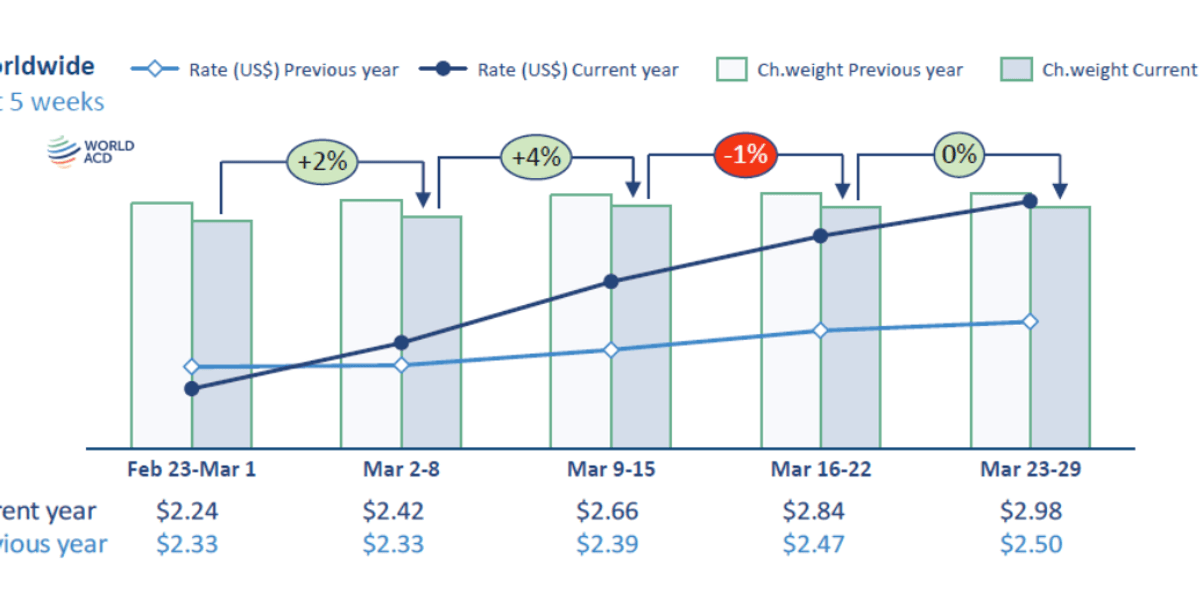

Late February: $95 per barrel. March 20: $197. Straight-up shock, tied to Iran’s war moves lighting oil markets ablaze. Airlines slap surcharges; ocean carriers pile on bunker fees. It’s not hype—Dimerco’s data shows Taiwan air freight rates climbing 20-30% on key lanes, North America lanes 20-50%.

Here’s the thing. Rerouting eats capacity. Planes dodge Middle East skies; ships skirt Hormuz risks. Southeast Asia exporters—Korea, Taiwan—feel the pinch first, bookings tighter than a drum.

Rail? China-Europe hubs tacked $300-500 per container in March. Now? Over $500 across the board as shippers flee ocean volatility.

“April is shaping up to be a cost-driven freight market, not a broad demand-driven one,” Catherine Chien, Chairwoman of Dimerco, said in a release. “We are seeing fuel shock and Middle East rerouting tighten air capacity from Taiwan, Korea, and across Southeast Asia, while ocean carriers layer in bunker-related surcharges and rail into Europe moves higher as shippers look for alternatives. If disruption around the Strait of Hormuz continues, shippers should expect elevated freight costs, shorter rate validity, and more route-specific volatility across Asia-Europe and Asia-North America in the weeks ahead.”

Chien’s not spinning corporate line—she’s calling the architecture shift. Freight’s decoupling from demand cycles, lashing to geopolitics and barrels.

Why Is Air Capacity from Asia Suddenly Scarce?

Planes can’t just vanish. But they do—when pilots balk at war zones, when insurers hike premiums 10x. Taiwan-Korea lanes? 20-30% rate hikes. North America? Double that, fuel surcharges fueling the fire.

Look. Post-Ukraine, we saw echoes—Black Sea blocks forced grain reroutes. Now Hormuz, carrying 20% of global oil, threatens the whole artery. Tankers idle; VLCCs (very large crude carriers) swing wide, adding weeks and costs.

Shippers pivot. Air for high-value (electronics, pharma). Rail for bulk to Europe. Ocean? Pray for no Hormuz blockade.

But wait—Dimerco flags softer manufacturing momentum. Not collapse, just drag. Higher ops costs mean thinner margins, forcing nearshoring talks to accelerate. (Remember 2021’s box crisis? This is that, geopolitically juiced.)

A single punch: This isn’t transient fog. It’s 1973 Oil Crisis redux—when OPEC embargo quadrupled prices, birthed just-in-time inventory myths, reshaped auto giants. Unique insight: Iran War’s doing the same for freight architecture. Expect permanent multimodality—air-rail hybrids as default, not exception. Dimerco’s PR stays measured, but they’re underselling the pivot: supply chains won’t snap back; they’ll evolve, costlier, resilient-er.

What If Hormuz Stays a Flashpoint for Months?

Short-term: Volatility city. Rates valid for days, not weeks. Asia-Europe ocean surcharges balloon; air bookings vanish.

Medium? Fuel at $200+ sticks if sanctions bite harder. Manufacturers stockpile—hello, inventory bloat. (Warehouses in Vietnam, Mexico? Filling fast.)

Bold prediction: By Q3 2026, 15% of Asia-North America volume shifts to rail-air combos, rates stabilizing 30% above baseline. Shippers who hedge fuel now win; laggards eat 50% hikes.

Corporate spin? Dimerco’s report dodges doomsaying—smart—but ignores the why beneath: decades of just-in-time fragility exposed again. Geopolitics isn’t footnote; it’s the new rate sheet.

And rail hikes? $500+ per TEU isn’t blip. Eurasian land bridge booms, but capacity caps loom—China’s Belt-and-Road rails choke under volume.

Shippers, wake up. Model for disruption, not demand.

🧬 Related Insights

- Read more: Project44 Gobbles LunaPath.ai: Second AI Bet in Four Years

- Read more: AI Chews Up Entry-Level Jobs — And Spits Out Tomorrow’s Leaders?

Frequently Asked Questions

What are the main Iran War effects on global freight markets?

Fuel prices doubled, air capacity tightened via rerouting, Hormuz threats spiking ocean surcharges—driving 20-50% rate hikes across air, ocean, rail.

How much have air freight rates increased due to the Iran War?

Taiwan lanes: 20-30%. North America: 20-50%. Blame fuel shocks and Middle East avoidance.

Will freight costs stay high if Strait of Hormuz disruption continues?

Yes—expect shorter rate validity, more volatility, elevated costs on Asia-Europe/North America lanes for weeks or longer.