Ships ghosting through the Strait of Hormuz like thieves in the night.

That’s the new normal, courtesy of Middle East tinderboxes. Descartes’ April Global Shipping Report drops the mic: global supply chain planning? It’s all risk management these days, baby. Flexibility’s the watchword amid this cocktail of volatility — think rockets, tariffs, and trade talks gone sideways.

And here’s the kicker. U.S. container imports roared back in March 2026 — up 12.4% from February’s slump, hitting 2.35 million TEUs. Still 32% above pre-pandemic glory days. But year-to-date? Lagging 2025 by 4.8%. Rebound? Sure. Rock-solid? Ha.

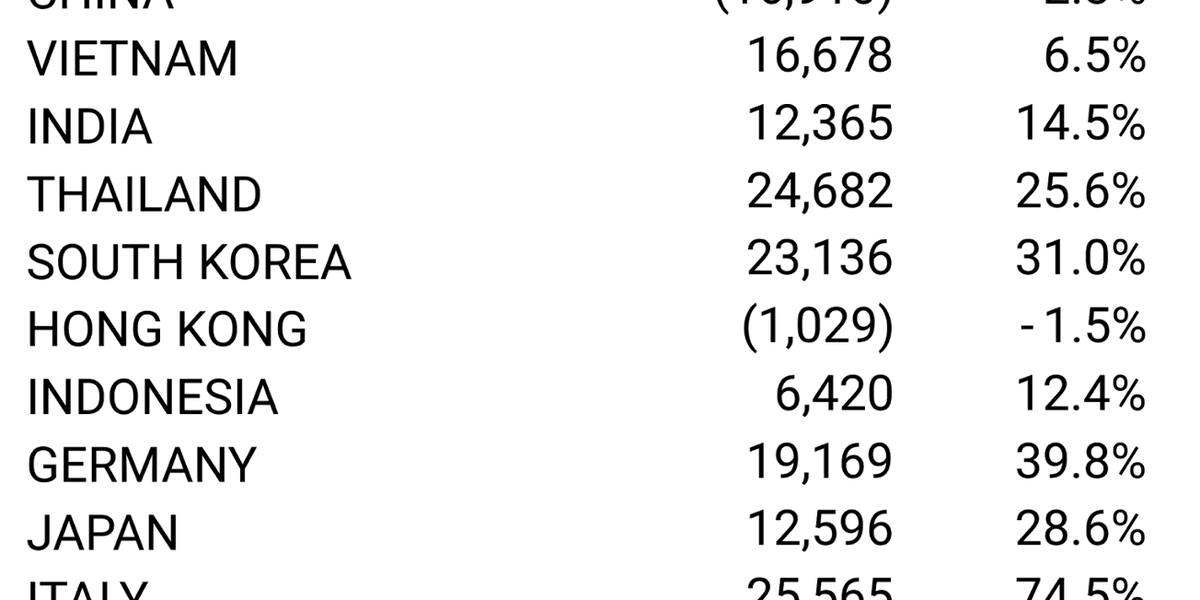

Top ten origin countries pumped out 8.2% more volume month-over-month. Italy? Exploded 74.5%. Thailand and South Korea not far behind. Germany, Vietnam, Japan, India — all strutting gains. China? The lone laggard, down 2.3%. Hong Kong dipped too. Smells like diversification fever, doesn’t it?

Why Importers Are Ditching China (Finally?)

Look, China’s slip isn’t shocking. Tariffs loom like storm clouds — U.S. policy’s a flip-flopping mess. Throw in EU, India, and China negotiations, and you’ve got executives mainlining antacids. But Italy surging 74%? That’s not wine exports; it’s rerouted goods, bets on safer lanes.

Jackson Wood, Descartes’ Director of Industry Strategy, cuts through the spin:

“While March import volumes remain near historically high levels and port operations continue to perform efficiently, escalating tensions in the Middle East, evolving U.S. tariff policy and shifting global trade dynamics are increasing volatility around routing, costs and sourcing decisions.”

Spot on. But let’s call the bluff: ports humming? Great. Until a drone swarm says otherwise.

Importers are scrambling — diversifying beyond China, tweaking routes to skirt war zones, leaning on data tech for quick pivots. Sounds smart. Feels desperate.

Will Middle East Tensions Snap Supply Chains for Good?

Bab al-Mandeb’s under siege. Hormuz? Practically a no-go. Key chokepoints turning into kill boxes. Remember 1973? OPEC embargo choked oil flows, sparked stagflation that lingered years. Bold prediction: this ain’t oil, but the parallel’s eerie — expect embedded inflation as rerouting jacks costs 20-30% on key routes. Descartes hints at it; I’m yelling it.

U.S. ports chug along — efficient, they say. But volatility’s the real beast. One Houthi hit on a tanker, and poof: surcharges skyrocket. Sourcing shifts to Thailand? Fine, until Vietnam floods or India strikes. It’s whack-a-mole geopolitics.

And the PR gloss? Descartes pushes its software as the savior — data-driven decisions in chaos. Fair play; tech helps. But don’t kid yourself: no algorithm outruns a missile. This reeks of vendor hype amid genuine panic.

Zoom out. Global trade’s not broken — yet. March volumes scream resilience. But risk management’s the North Star now. Flexibility? It’s code for ‘pray and pivot.’ Ports like LA/Long Beach handle the load, but cracks show: YTD imports trail last year. China’s wobble? Symptom of bigger disease.

Here’s the thing.

We’ve seen this movie. Post-9/11, chains bulked up buffers. COVID? Near-death experience. Now Middle East redux. Unique insight: unlike pandemics, this is perpetual simmer — no off-ramp soon. Iran proxies won’t quit; U.S. elections could torch tariffs higher. Prediction: by Q4 2026, diversified sourcing adds $50B+ to U.S. import costs. Hidden tax on consumers. You’re paying it at Walmart.

Dry humor aside — it’s grim. Importers brag efficiency; reality’s a knife-edge. Descartes nails the data, but their cheery ‘use technology’ line? Eye-roll. Tech’s a crutch, not a cure.

Top origins flexing: Italy’s boom (25k TEUs extra) — luxury goods? Electronics rerouted? Who knows. Thailand’s 25% jump screams auto parts shuffle. Korea, Germany: machinery muscle. Vietnam steady climber. India’s 14.5%? Textiles, pharma hedging bets.

China’s 2.3% drop (17k TEUs less)? Not apocalypse, but signal. Hong Kong’s blip too. Trade lanes fracturing.

Ports? Efficient machines — for now. But escalating risks demand more than dashboards. Real talk: boards need war-gaming sessions, not just KPIs.

How Bad Could U.S. Tariffs Get This Time?

Tariff flux — Trump’s ghost or Biden’s legacy? Flux anyway. Negotiations with EU/India/China? Stalled drag races. Add Middle East fuel to fire, and routing costs spike. Sourcing decisions? Gut-check time.

Descartes urges data use. Fine. But here’s the acerbic truth: companies chased cheap China for decades, ignored risks. Now paying premium for ‘resilience.’ Schadenfreude? A tad.

March rebound seasonal — post-Lunar New Year surge. But elevated vs. 2019? Pandemic distortions linger. True test: sustained volatility.

**

🧬 Related Insights

- Read more: GOP Slams Door on Iran War Powers as Oil Chokepoints Loom

- Read more: Melania Trump’s ‘Love, Melania’ Email to Maxwell Fuels Endless Epstein Whispers

Frequently Asked Questions**

What are the main risks to global shipping from Middle East tensions?

Strait of Hormuz restrictions, Bab al-Mandeb threats — chokepoints for 20%+ of world oil, massive container traffic. Disruptions mean skyrocketing freight rates, delays.

How have US container imports changed in 2026?

March up 12.4% MoM to 2.35M TEUs, 32% above 2019. But YTD down 4.8% vs 2025. Rebound amid risks.

Is China losing ground in US imports?

Yes — down 2.3% in March from top origins. Diversification to Italy, Thailand, others accelerating.