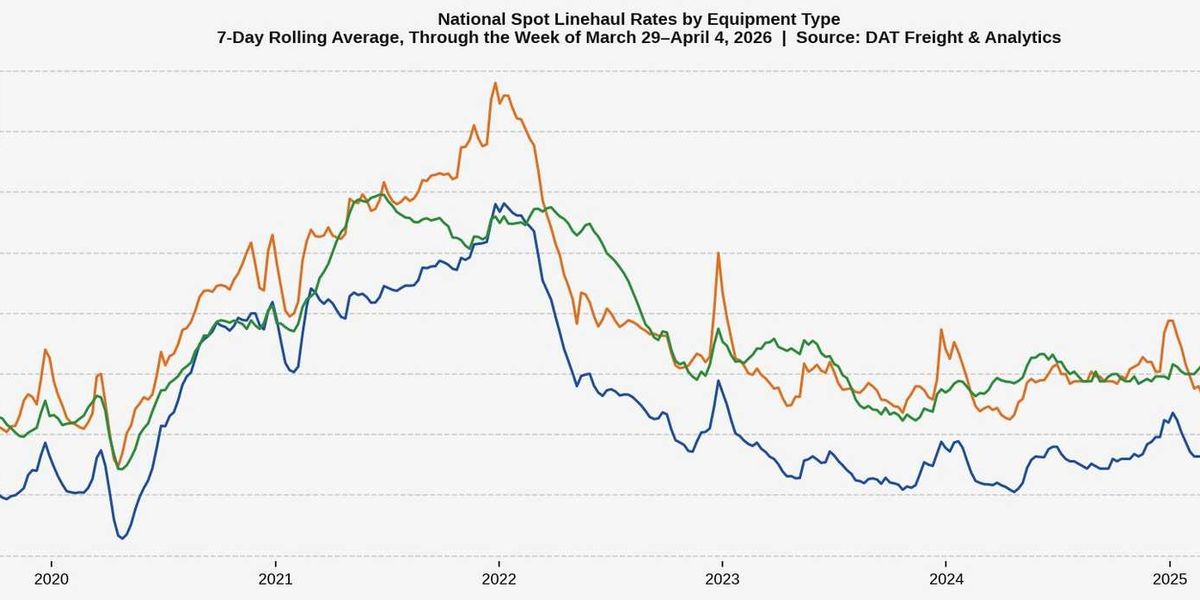

The blinking cursor on the dispatcher’s screen reflected a familiar, yet increasingly strained, reality. March 2026. A month where the numbers on the U.S. Bank Freight Payment Index didn’t just tick up; they rocketed skyward, defying the gentle, almost stagnant, ebb and flow of actual freight volumes.

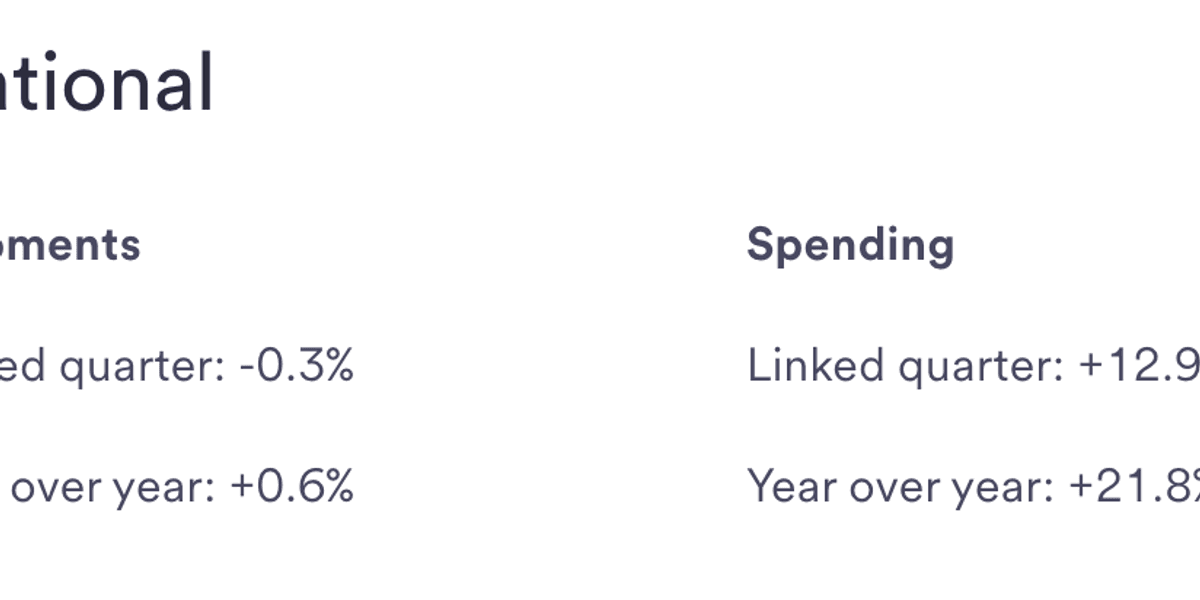

Here’s the kicker: shipper spending on freight services shot up a staggering 12.9% from the previous quarter, reaching heights not seen since the chaotic latter days of 2020. All this, while the volume of goods being shipped nationwide saw a negligible 0.3% dip. Think about that for a second. More money being paid for essentially the same amount of stuff being moved. It’s the classic sign of a market where the supply side is screaming and the demand side is barely whispering.

This isn’t your typical economic indicator dance, where strong spending usually tracks with a booming volume of goods. No, this is different. This is a market being reshaped by scarcity, not by an insatiable appetite for consumer goods. The culprit, according to the U.S. Bank Freight Payment Index, is a potent cocktail of tightening capacity and a sharp surge in diesel fuel prices. The latter contributed, sure, but the real heavy lifting comes from the sheer lack of available trucks.

“This is a market being reshaped by supply, not demand,” said Bob Costello, senior vice president and chief economist at the American Trucking Associations. “The increase in rates and shipper spending reflects a rare supply-side recovery, with little change in freight volumes and simply fewer trucks competing for freight.”

Costello’s assessment is sharp and to the point. We’re witnessing a “supply-side recovery” – a term that sounds almost counterintuitive in a world obsessed with demand-side stimulus. It’s a scenario where fewer carriers are battling for a relatively static pool of freight, inevitably driving prices up. The prolonged industry downturn has clearly pruned the number of active trucks, and now, the remaining players are reaping the rewards.

The Regional Divide (and Unity)

While the national picture is clear, regional data reveals a bit more nuance, though the overarching trend of increased spending remains stubbornly consistent. The Midwest and West regions saw sequential shipment gains, a positive sign for those areas. Conversely, the Southwest, Southeast, and Northeast experienced declines in volumes. Yet, across all five regions U.S. Bank tracks, shipper spending climbed. This broad-based increase underscores that the capacity crunch isn’t a localized phenomenon; it’s a nationwide challenge.

Why Does This Matter for Shippers?

Bobby Holland, director of freight business analytics at U.S. Bank, nails the core problem for businesses trying to manage their logistics budgets. “What makes this quarter stand out is how abruptly costs moved higher even though freight activity itself didn’t,” he noted. For companies that rely on predictable volume signals to forecast their transportation spend, this creates a decidedly “much harder environment to plan and budget.” The usual indicators are off, replaced by an unpredictable cost structure influenced by factors beyond their direct control.

The surge in fuel prices in March certainly added a layer of volatility, but Holland emphasizes the more profound takeaway: “the pricing dynamics shifted faster than demand conditions.” This isn’t a slow burn; it’s a rapid repricing event driven by structural supply constraints. It’s a stark reminder that in logistics, sometimes the most significant market shifts aren’t about moving more goods, but about how many vehicles are available to move them.

This data also represents a subtle, yet significant, architectural shift in how the freight market is operating. For years, the narrative has been about optimizing routes, driving down fuel consumption, and increasing driver efficiency – all demand-side or operational improvements. Now, the focus is being forced back to the fundamental supply structure of the industry. The number of available trucks, the cost of operating them, and the willingness of carriers to stay in business are the dominant forces. Companies that don’t grasp this will find themselves perpetually playing catch-up, their budgets blown by a market that’s less about volume and more about access.

This isn’t just a quarterly blip; it’s a harbinger of a potentially tighter, more expensive future for shippers. The days of readily available capacity and predictable freight rates might be over, at least for the foreseeable future. The question now isn’t if shippers will pay more, but how they’ll adapt to a market fundamentally dictated by who has the trucks.