Here’s the deal for everyday folks: your package might take a smidgen longer, or cost a bit more, if it’s the kind of low-margin freight UPS no longer wants. Forget the days of carriers begging for every box, any box. UPS isn’t playing that game anymore.

And honestly, who can blame them? The economics have tanked. We’re talking about a fundamental recalibration, a strategic pivot that’s less about hitting arbitrary volume targets and more about actual, tangible profit. In the first quarter of 2026, UPS saw U.S. Domestic revenue dip 2.3 percent year-over-year, yet revenue per piece shot up 6.5 percent. That’s not a typo. Less volume, more money per package. Simple, brutal math.

Is Volume Even a Dirty Word Anymore?

For years, the parcel world ran on volume. More packages meant better utilization, fatter margins. It was a simple equation. But that equation’s been scrubbed clean. UPS is actively shedding less profitable business, most notably, that of Amazon. They’ve slashed average daily Amazon volume by half a million pieces this quarter and plan to cut it by another chunk soon. Amazon’s slice of UPS revenue? Down from 10.6% to 8.8%. This isn’t a minor adjustment; it’s a full-blown network remix.

The new mantra? Higher-quality volume, better yield, more predictable network flows, and customers who actually fit UPS’s cost structure. It’s a switch from ‘grow at all costs’ to ‘grow smart.’

Why the Network Is Getting Tighter

Labor costs aren’t exactly shrinking, and routing complexity is only getting worse. Deliveries are more spread out, yet customer expectations? Still sky-high. So, UPS is tightening the screws. They’ve already racked up $600 million in cost savings just in the first three months of 2026, and there’s more where that came from. This discipline shows up everywhere: aligning capacity with demand, dumping low-yield freight, closing or combining facilities, shoving more automation into their hubs, and aggressively managing route efficiency. Expect more UPS parcel facilities to shutter this year. These aren’t temporary bandaids; these are structural shifts.

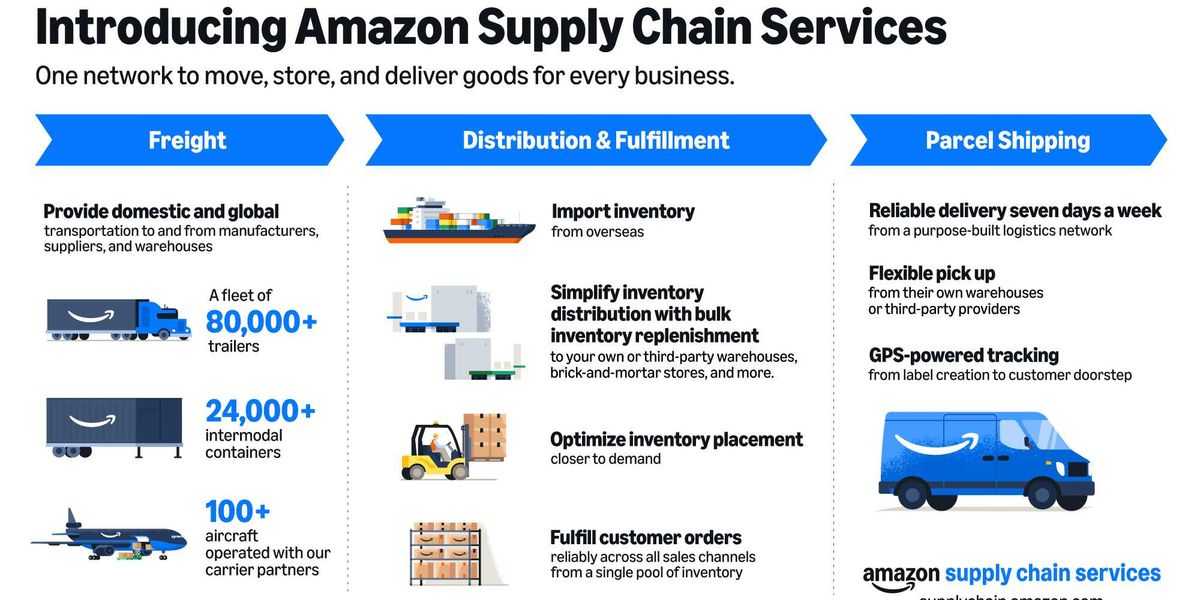

Amazon: Frenemy Edition

Here’s another twist: Amazon isn’t just ditching UPS; it’s becoming a direct competitor. Through Amazon Supply Chain Services, they’re now offering storage, shipping, fulfillment, and delivery to other businesses. This puts Amazon square in the ring with UPS and FedEx. For UPS, this isn’t just about managing a big customer; it’s about fending off a formidable rival that’s using its own logistics infrastructure as a platform. It underscores why protecting yield and focusing on profitable segments is non-negotiable.

“The parcel market is being reshaped by a large shipper that has become a logistics platform in its own right.”

The Data-Driven Delivery Dance

Parcel networks are getting a serious digital makeover. Planning cycles are shrinking, and decisions are being made much closer to real-time. Route plans get updated more frequently, capacity is flexed in smaller increments, and linehaul decisions are increasingly dictated by data. Sortation assets are deployed based on tighter volume assumptions. This is where optimization shifts from a whiteboard exercise to real-time execution. Think RFID labeling, cold chain services, and even same-day delivery through partnerships like Roadie. It’s all about moving the right packages through the network, not just more packages.

What This Means for You (the Shipper)

For businesses that ship stuff, the ground is shifting. Carrier relationships are becoming choosier. Contracts will focus more on lane fit, density, service profile, and yes, profitability. Predictable volume and clean tender patterns will become gold. Relying on a single carrier? That’s looking riskier by the day. And guess what? Shippers who share better data—demand forecasts, returns info, seasonal swings—will be the ones who get preferential treatment. The old game of ‘take all the volume’ is over. The new game is ‘take volume that makes us stronger.’

This isn’t a temporary blip; it’s a fundamental reset of the parcel market. The era of the volume chase is over. Welcome to the age of disciplined, yield-focused logistics. And for those of us who’ve been watching Silicon Valley for two decades, this smells like a much-needed dose of reality hitting the logistics world. Finally.