Ever wonder why your Amazon order still shows up on time, even with bombs falling near the Strait of Hormuz?

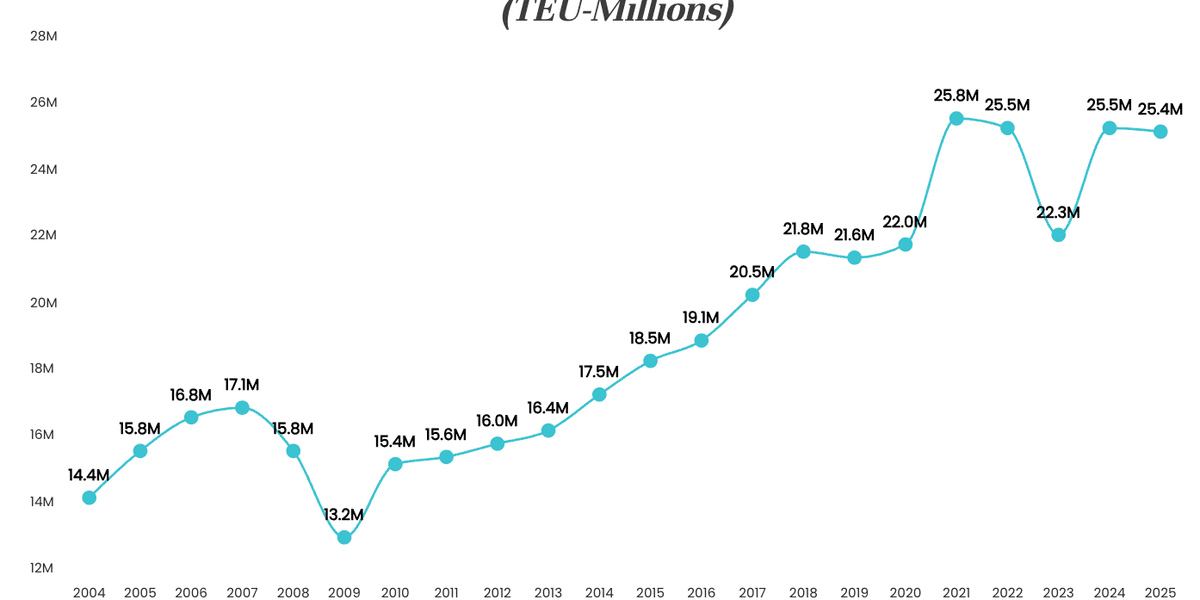

U.S. imports held steady in February despite the Iran war—or whatever we’re calling this mess now. Global Port Tracker from NRF and Hackett Associates says container volumes at major ports hit 1.95 million TEUs. Down a bit from January, sure, but nothing screams panic. Traditional Lunar New Year slowdowns get the blame, not missiles.

Here’s the kicker. Ocean carriers are choking on fuel costs. Strait restrictions jack up tanker prices, and suddenly every container ship pays more to chug across the Pacific. Retailers? They’re sweating bullets.

Why Aren’t Ports Freaking Out Yet?

Look, U.S. doesn’t suck up much container cargo from the Middle East. Ben Hackett nails it: tariffs already slowed things, Iran? Barely a blip operationally. But fuel—oh, fuel’s global. “The United States is less impacted operationally as there is no shortage of fuel at U.S. ports, but the price of fuel here is based on international pricing,” Hackett warns. Higher costs mean pricier shipping. Inflationary, he calls it. Code for: your grocery bill climbs.

Asia’s ports? They’re thirstier. Persian Gulf fuel keeps their ships humming. Shortages loom if this drags. Ceasefire? Too soon to cheer. And consumers? Gas prices sting already—less cash for impulse buys.

“Just because retailers don’t import a lot of merchandise from the Middle East doesn’t mean the U.S. supply chain isn’t affected by the turmoil there,” NRF Vice President for Supply Chain and Customs Policy Jonathan Gold said in a release. “The supply chain is global and disruptions anywhere along it can have ripple effects whether it’s rerouting of vessels, equipment out of position, higher fuel costs for shippers, or rising gas prices that leave less money in consumers’ pockets. Retailers are monitoring the situation on a daily basis and working with their transportation partners to minimize any impact. In the meantime, retailers continue to face rising tariffs and continued trade policy uncertainty that put downward pressure on imports and upward pressure on prices.”

Gold’s right—it’s all connected. But let’s call the bluff: retailers “monitoring daily”? That’s PR spin for “praying it doesn’t hit earnings calls.”

Will Trump’s Tariffs Turn This Into a Perfect Storm?

Trump’s not helping. Last month: 10% global tariff via Trade Act—SCOTUS nixed the emergency powers trick. Last week? Tweaks to steel, aluminum, copper Section 232s, plus pharma hits. Liberation Day tariffs from ‘25 still echo, tanking May-June last year.

Projections? March: 1.97 million TEUs, down 8.3% YoY. April 2.08M (-5.6%), May 2.09M (+7.3%—weak comps), June 2.1M (+6.9%), July 2.2M (-8%), August 2.18M (-6%). First half ‘26: 12.3M TEUs, -1.8% from ‘25.

Numbers whisper slowdown. Tariffs bite imports, fuel amplifies. My hot take? This reeks of 1973 oil embargo vibes—remember stagflation? Nixon’s price controls flopped, lines at pumps stretched miles. Bold prediction: if Hormuz stays dicey through summer, we see 10-15% shipping surcharges by Q3. Retailers pass it on; Walmart hikes socks 20 cents, you grumble. Supply chains reroute—hello, longer lead times from Vietnam detours.

Skeptical? Me too. NRF paints resilience, but they’re retail shills. Hackett’s clearer: ripple effects everywhere. Equipment misplaced, vessels dodging hot zones—costs compound. And Trump’s tariff whiplash? Pure chaos. Adjusting Section 232s mid-war? It’s like rearranging deck chairs on a tanker.

Ports chug on—NY/NJ data pending, but trend’s soft. February’s 7.5% monthly drop? Seasonal, they say. YoY 4.2% dip? Blame tariffs, not Tehran. Yet fuel’s the sleeper hit. International pricing means no escape. Shippers balk at rates; spot market already twitching 5-10% north.

Unique angle: history rhymes. ‘79 Iranian Revolution spiked oil 150%. Containers were niche then, but lesson holds—global chokepoints crush margins. NRF glosses this; I’m calling it: expect supply chain stagflation by fall. Retailers hoard inventory now? Smart. Consumers? Stock up on cheap gas while it lasts.

Dry humor aside, this isn’t doom porn. But ignoring fuel-tariff combo? Foolish. Carriers pass costs; retailers squeeze suppliers; prices creep. Your next iPhone case? Five bucks pricier, thanks to Hormuz.

The Road Ahead: Bracing for Bumps

March-April look grim YoY. May-June rebound off lousy ‘25 baselines. But July-August slide again. War wildcard: Asian fuel crunch could idle factories. U.S. ports stocked—for now.

Retailers pivot: more nearshoring talks, but Mexico’s no panacea with auto strikes looming. Trump’s pharma tariffs? Drug prices jump—hello, election year headaches.

Bottom line? Steady imports mask brewing storm. Fuel’s the fuse; tariffs the accelerant. Watch spot rates like hawks.

🧬 Related Insights

- Read more: Middle East Missile Dodge: Global Trade’s Risk Obsession Hits Fever Pitch

- Read more: Trump Blasts Iran’s Strait of Hormuz Tolls as Tankers Rot and Prices Spike

Frequently Asked Questions

How is the Iran war affecting U.S. imports?

Fuel costs for ships are surging due to Strait of Hormuz issues, even if direct cargo from the region is minimal. Tariffs add pressure.

Will Iran conflict fuel prices raise retail costs?

Yes—higher shipping expenses get passed to consumers, potentially inflating prices 5-10% on imports.

What do Global Port Tracker forecasts say for 2026?

First half at 12.3 million TEUs, down 1.8% YoY, with fuel and tariffs dragging volumes.